Mortgage Securitisation...is it Legal?

Mortgage Securitisation...is it Legal?

Or is it a Racket?

Mortgage Securitisation: From Originator to Investor Profits

Mortgage securitisation is a financial process that transforms a pool of individual home mortgages into marketable securities, which can be sold to investors.

This is quite a complex mechanism, but banks do it as it provides them with liquidity (more cash) and it also creates new investment opportunities across varying risk profiles.

This particular post delves into how banks securitise your mortgage, the role of brokers, the transition of your bank from originator to servicer, and the profit potential for investors purchasing mortgage-backed securities (MBS) tranches.

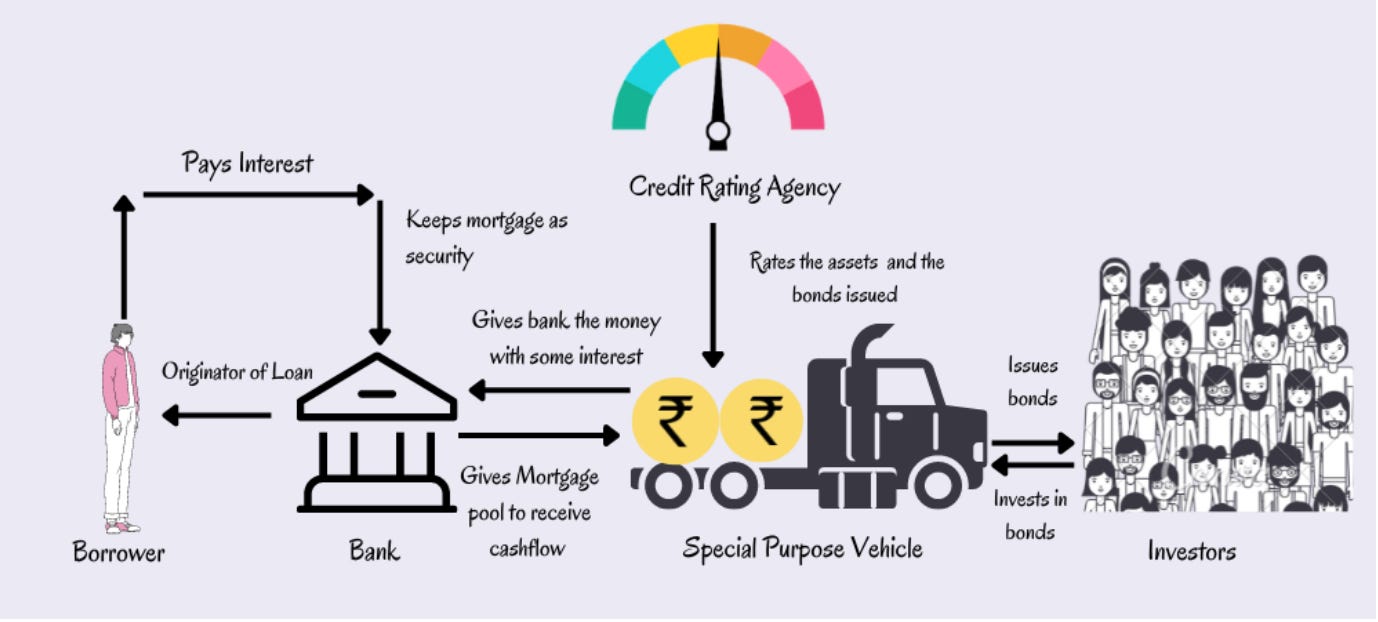

The Mortgage Securitisation Process

1. Origination: The process begins with the origination of mortgages by banks or financial institutions. Homebuyers apply for loans, and the bank underwrites and funds these loans after evaluating the creditworthiness of the applicants. (Where the bank gets the money from is another story for another article…but it’s not from deposits!)

2. Pooling: Once your loan has been “originated”, which takes about 3 months, the bank bundles your mortgage with multiple other mortgages into a pool. These pools typically consist of mortgages with similar characteristics such as interest rates, loan terms, and credit quality.

3.s: The pooled mortgages are then sold to a special purpose vehicle (SPV), a legally separate entity created to facilitate securitisation. The SPV issues mortgage-backed securities (MBS) backed by the pool of mortgages.

4. Tranching: The MBS are structured into tranches, or slices, which vary in terms of risk and return. These tranches are categorised into senior, mezzanine, and equity tranches, each offering different levels of priority in the cash flow distribution from the underlying mortgage payments.

The Role of Brokers in Securitisation

Brokers play a crucial role in the distribution of MBS to investors. Their functions include:

- Underwriting: Brokers assess the value and risk of the MBS, determining the pricing and terms under which the securities will be offered to investors.

- Marketing and Sales: Through their networks, brokers market the MBS to institutional and individual investors. They highlight the benefits of the securities, such as the expected yield and risk profile.

- Advisory Services: Brokers often provide advisory services to investors, helping them understand the complexities of MBS and guiding them in selecting appropriate tranches based on their risk tolerance and investment objectives.

Transition from Originator to Servicer

Once the mortgages are securitised, the originating bank often transitions to the role of the servicer. As the servicer, the bank is now responsible for managing the day-to-day operations of the mortgage pool, including:

- Collecting Payments: The servicer collects monthly mortgage payments from borrowers and ensures timely distribution to investors based on their tranche.

- Customer Service: They handle borrower inquiries, manage escrow accounts, and provide customer support related to the mortgage.

- Delinquency Management: The servicer manages delinquent loans, negotiating with borrowers, initiating foreclosure proceedings if necessary, and attempting to recover as much of the outstanding debt as possible. This can be tricky for them if they have been proven to have sold the security, simply because they no longer have what’s known in law as locus standi. They do not have title and interest to collect any outstanding debt. They get round this by leaving their name on the security at the Land Registry. However, this is unlawful as the holder of the security is now the investor Company and their name should be on the deeds.

Investor Profits from Buying Tranches

Investors buy tranches of MBS to achieve their specific investment goals. Here’s how they make money:

1. Interest Payments: Each tranche receives a portion of the monthly mortgage payments, which include both principal and interest. Senior tranches typically receive payments first, offering lower risk but also lower returns compared to subordinate tranches.

2. Principal Repayments: As borrowers pay down their mortgage principal, these payments are passed through to investors. The schedule and priority of these repayments depend on the structure of the tranches.

3. Credit Enhancement: Some tranches benefit from credit enhancements such as over-collateralization, excess spread, and insurance, which provide additional security and can enhance the tranche’s credit rating, making it more attractive to investors.

Risk and Return in Tranches

The structure of tranches is designed to cater to different risk appetites and return expectations:

- Senior Tranches: These tranches are first in line for payment and thus have the lowest risk. They typically offer lower yields but provide a more stable and predictable cash flow.

- Mezzanine Tranches: Positioned between senior and equity tranches, mezzanine tranches offer a balanced risk-return profile. They receive payments after senior tranches and before equity tranches.

- Equity Tranches: Also known as the “first-loss” tranches, these are the riskiest but offer the highest potential returns. They are last in line for payment and absorb initial losses from defaults within the mortgage pool.

Market Dynamics and Investor Strategies

The attractiveness of MBS tranches to investors depends on several market factors, including interest rates, housing market trends, and overall economic conditions. Investors employ various strategies to maximize returns and manage risk:

- Diversification: By investing in multiple tranches across different MBS, investors can diversify their risk exposure and stabilize returns.

- Hedging: Investors use financial instruments like interest rate swaps and options to hedge against interest rate fluctuations and other risks.

- Active Management: Institutional investors, such as mutual funds and pension funds, actively manage their MBS portfolios to capitalise on market opportunities and mitigate risks.

Conclusion

Mortgage securitisation is a sophisticated financial process that benefits both banks and investors. Banks can transform illiquid assets into liquid securities, freeing up capital to issue more loans. Investors, on the other hand, gain access to a range of investment opportunities with varying risk and return profiles through MBS tranches. Brokers facilitate this process by underwriting, marketing, and selling the securities, while the originating bank often continues to manage the mortgages as the servicer.

To find out if this has been done properly, you should send a Data Subject Access Request to your bank or mortgage provider.